Late spring, I discussed the anticipated opportunity for estate and gift planning given the favorable business valuation and tax regime climate (previous article). We have learned a lot since then, and although business valuations are still somewhat soft, the focus has shifted more towards the extreme uncertainty of whether a tax climate that benefits successful business owners with the ability to shield significant portions, if not all, of their assets from estate tax is going to remain beyond this year.

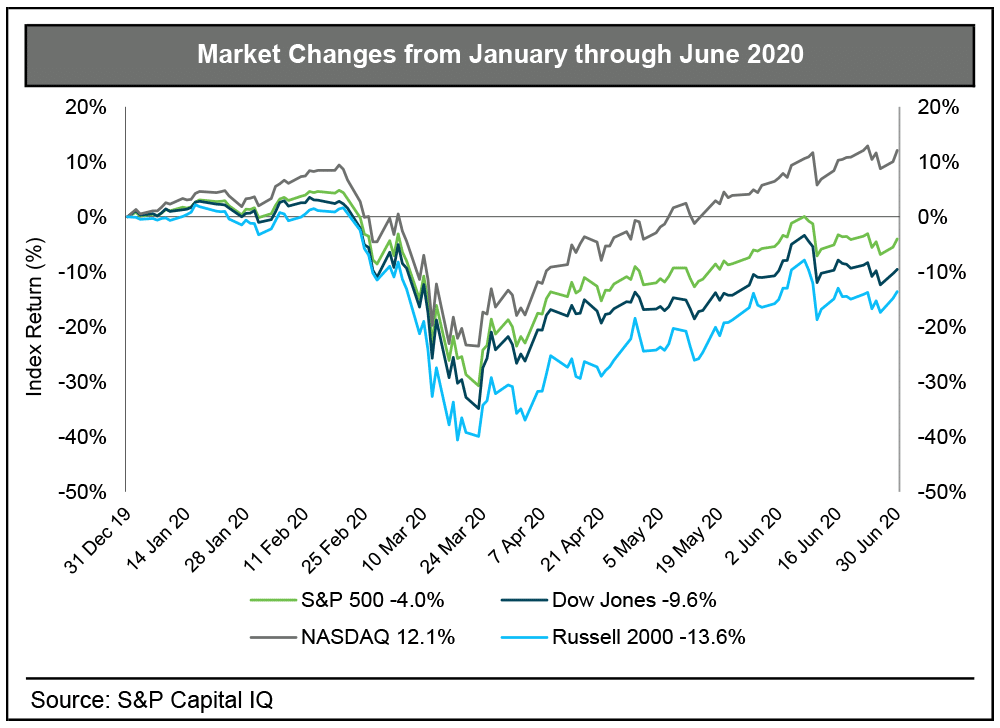

Since March, the federal government has pumped approximately $3.3 trillion dollars of stimulus monies into the American economy. As a result, the short-term impacts on the economy have largely been positive. Financial markets have almost completely recovered from the dip experienced in March with the Russell 2000 indicating a 13.6% decline from the beginning of the year until the end of June, compared to the nearly 31.0% decline through Q1. What we are finding is that after an initial pause to assess and cautiously analyze deal terms and company outlooks, M&A activity has continued. As such, business valuations, as of now, are holding relatively steady for many of the lower-middle-market clients our firm serves. The graph below illustrates the market changes through the first two quarters of 2020.

What we are seeing now is not necessarily an opportunity to act upon lower business values, but potentially a shorter window to take action on estate planning. Political, economic, and fiscal trends are placing tremendous pressure on the need to generate additional tax revenue, regardless of the results of the upcoming Presidential election. The continuation of the current, favorable tax policies is uncertain, and the survival of the current gifting exemptions is at stake. Under U.S. federal tax law, the current lifetime gifting exemption is the highest it has ever been at $11.58 million per individual, and $23.16 million for a married couple. If gifts exceed these exemption limits, the excess is taxed at a flat 40%. Prior to the Tax Cuts and Jobs Act (TCJA) in 2017, the federal gift and estate tax exemption was less than half of what it is today under current tax law. Also consider the tax regime at a comparable time in our economic cycle, 2007, where the exemption was $1.5 million with a maximum excess tax rate of 45.0%.

If business owners are not prepared now, a significant change in tax law could result in costly tax consequences that significantly alter estate plans. If the current tax regime is replaced later this year to support the increased federal debts, business owners and advisors will benefit from having a plan in place to act while there is still time.

What to do to prepare:

Work with your advisors to understand the tax and cash flow implications of your estate plans while the higher exemptions are still available.

- If you have already considered making a gift, work with your advisors to understand and make an informed decision on whether it is in your best interest to make a gift now under the current tax law.

- If you have not yet considered gifting as a path to succession in the short-term, but see it as a long-term option, work with your advisors to understand the timing consequences.

What if your business is not worth $11.58 million?

Well, consider a situation where the exemption changes to a threshold similar to that of 2007, at $1.5 million. At this lower exemption level, a far greater number of businesses will be impacted. While we may not know the future outcome of the estate and gift tax exemption levels, it has become clear that due to increased fiscal pressures placed by Federal stimulus packages, taxpayers should, at minimum, be aware of the potential of reduced exemption levels on the horizon. Changes in future tax policies are uncertain, but if now is a viable option to accelerate succession plans, it is worth exploring the tax benefits.

Take action and work with your attorney, CPA, and/or wealth advisor to get prepared and become informed so that you can execute your estate plan in a manner that is most effective for you, your family, and your business.

If your plan involves gifting an interest in a closely-held entity, the IRS requires that the reporting of the gift for gift tax purposes be supported by a credible independent valuation. Our team has decades of experience preparing independent business valuations that withstand third-party scrutiny. If you have any questions regarding your gift and estate plans, we welcome an opportunity to be a resource to you and your advisors.

For more reading on this topic, you might also enjoy Nick Adamy’s article about the “soft” side of wealth planning.