If business owners didn’t already have enough reasons to make estate planning moves before the end of the year (see the excellent article my colleague, Kaylee Simerson wrote on that topic here), Here is another reason: valuation discounts are the highest they have been in over a decade. The reason for this is volatility. After a decade of relative calm in stock markets, volatility is back in a big way. But, what does stock market volatility have to do with valuation discounts? The answer, it turns out, is a lot.

Valuation discounts for estate planning revolve around control and marketability. While both discounts are up in the current market, we’ll focus this discussion on marketability.

Marketability is the ability to monetize an asset at any time. Publicly-traded stock enjoys this feature, while a private stock does not. There is value in this ability, which is why private stock trades at a discount to an otherwise identical public stock.

You can imagine that the ability to sell a stock at any time becomes more valuable when the price of that stock is swinging wildly. And, that is exactly what has been happening since the full impact of COVID-19 hit markets this spring. Continued political tensions, fear of a winter wave of new infections, geopolitics, and the effects of stimulus are all driving continued volatility this fall.

The value of marketability can be directly observed in the prices of at-the-money put options on public stocks. A put option gives the holder the right to sell at the strike price at any time up to the date of expiration. When the strike price of a put option equals the current trading price of the stock (i.e. “at-the-money”), the price of the option as a percentage of the underlying stock price gives us a good proxy for the value of marketability. And, that tells us what kind of discount the market would apply for a private stock that lacked such marketability.

Discounts for lack of marketability for private company stock tend to be higher than the discounts derived from put options because of longer and indefinite holding periods, restrictions on transfer, and company-specific reasons. Nonetheless, put options can provide a starting point when considering the discount for a private stock.

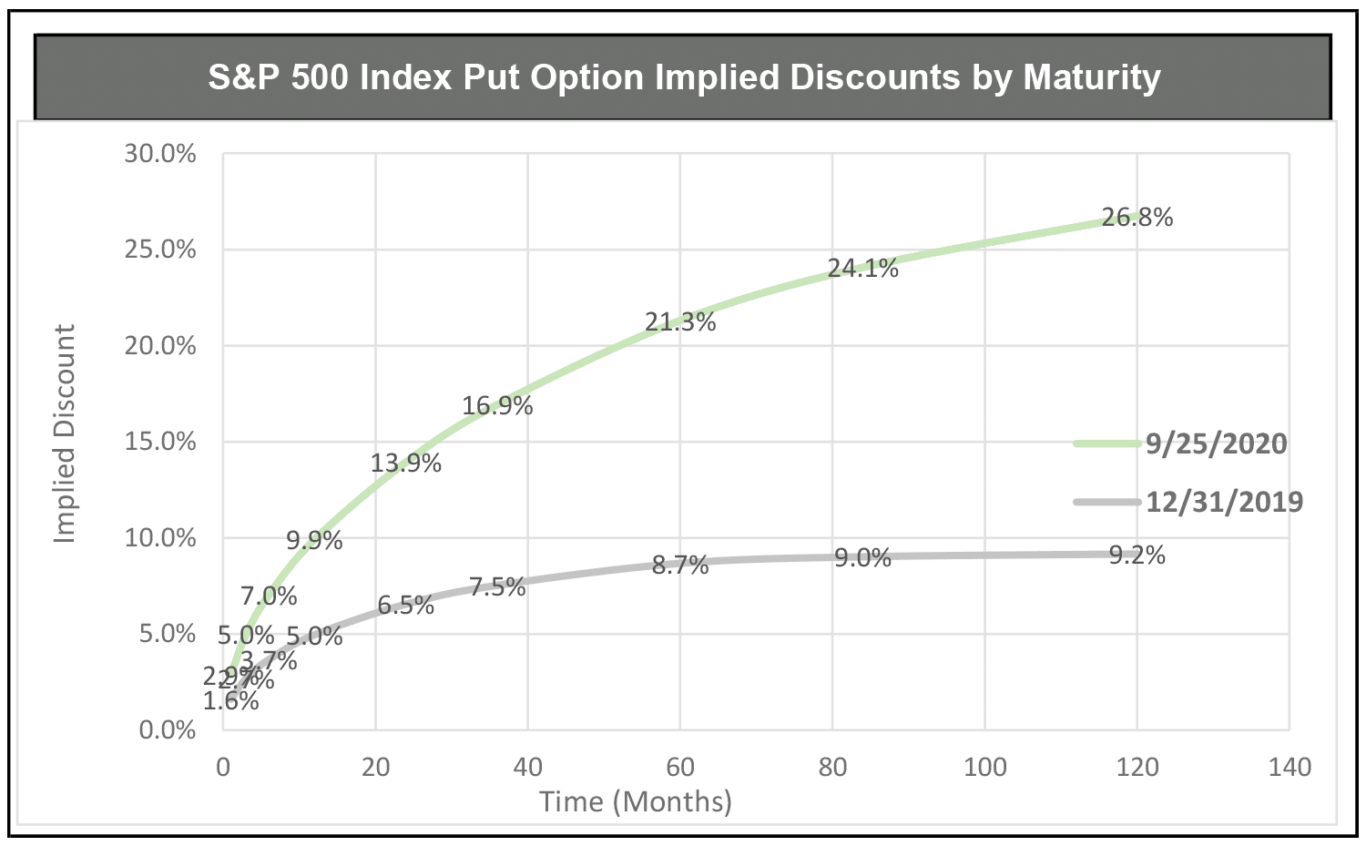

Since the end of last year, we have observed implied marketability discounts more than doubling, and in some cases nearly tripling, as a result of market volatility. The chart below summarizes discounts implied by put options for the S&P 500 as of December 31, 2019 and as of September 25, 2020. The difference is stark.

Obviously, the discount can vary from company to company. This is why a robust analysis of the subject company is a core part of a defensible valuation.

Contact us today

To learn more about how a valuation from Adamy can help you serve your clients with estate planning, contact one of our valuation experts.