The great partnership, a business model rooted in the 19th Century Gilded Age, has been losing favor among professionals since the 1990s. In the wake of the pandemic, the convergence of technology disruption, talent shortages, and Boomer retirements is driving professional service firms to find new ownership models to meet the changing needs of business.

For accountants, lawyers, architects, engineers, investment bankers, and countless niche professionals, the partnership was the primary model of ownership for over a century.

Two core features distinguish a partnership: 1) Owners are actively involved in the business, usually in leadership and revenue-generating roles; 2) Owners are entitled to a pro rata share of firm profits, instead of salary and bonus.

This is partially enshrined in the tax code, which generally prohibits partners from being treated as employees for tax purposes. This means that partners cannot take W-2 wages or bonus, and they are taxed on their proportion of the firm’s taxable income.

While this feature is formalized for entities taxed as partnerships, many professional service firms structured as corporations are run to effectively pay all profits to owners in the form of salary and bonus, in the spirit, if not technically the form, of the partnership model.

The partnership model was the dominant form of ownership for professional service firms throughout the 20th century. Changes in the economy and society in the 21st century have led firms to seek new ownership models that support the changing needs of modern firms. To learn where firms are headed, read on.

What’s Next? New Ownership Models for Professional Services

No single model has emerged to replace the partnership. Instead, leaders are developing new ownership models with three main priorities in mind: 1) Talent attraction and retention; 2) Ability to invest in growth; and 3) Operational flexibility.

While solutions vary across firms, all models share one key difference from the partnership model: Ownership is decoupled from both compensation and leadership.

This fundamental change is essential to provide flexibility to support diverse strategies and cultures necessary to thrive in a dynamic business environment.

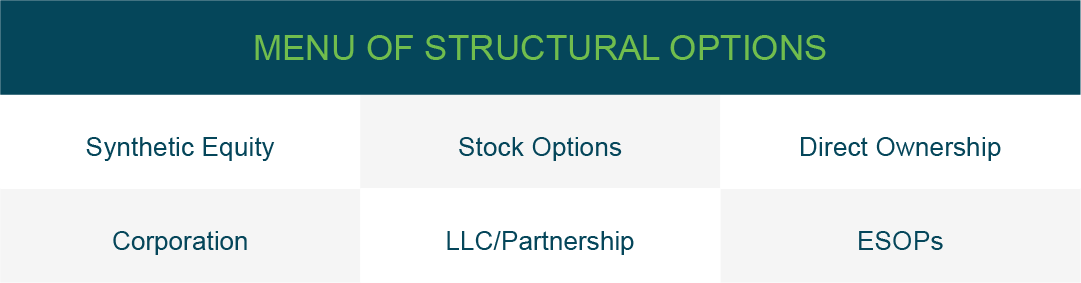

Ownership Structures

Once ownership is decoupled from compensation and leadership, a variety of different structures become available. Leaders are mixing and matching from a menu of structural elements to align with firms’ specific cultural and strategic goals.

Ownership as a Talent Attraction and Retention Tool

The ability to attract and retain talent has become the biggest obstacle to growth for many professional service firms. As a result, firms are looking for ways to grant ownership to employees much earlier in their careers. Instead of the all-or-nothing “making partner” carrot, firms are using a variety of equity incentive structures to allow employees to gain ownership early and build equity over their career.

Nearly all of the menu options, from “synthetic” equity plans, stock options, direct ownership, and highly-structured employee stock ownership plans (ESOPs) have important implications for talent attraction and retention.

Synthetic equity plans (sometimes called “phantom stock” plans) are a form of compensation that is based on the equity value of the firm. An important feature is that these plans do not grant legal ownership to the participant. A common form is a stock appreciation rights plan (SARs) that provides a payout after 3-5 years based on the appreciation of the value of the firm over that time.

These plans have the benefit of aligning employee incentives over a longer term than that of a typical bonus plan. However, the term is still short relative to the time horizon of direct ownership, and these plans are usually limited to top management, rather than rank-and-file employees. Further, the payout is taxed as ordinary income, without the potential for more favorable capital gains treatment. Because of these drawbacks, synthetic equity plans are most often used to supplement other broad-based incentive and ownership plans, providing more “juice” for key executives.

Stock options are often used as an alternative to SARs to achieve similar goals. A stock option allows the employee to buy stock at a set price (the strike price) in the future, usually up to 3-5 years. The strike price is set at the market value of the stock when the option is issued. When the employee exercises the option by purchasing stock at the strike price, they benefit from any appreciation in the price since it was issued.

Stock options are popular with public companies which enjoy a market to cash out options. They are also popular with private equity-backed companies that have plans to sell in a few years. Without these paths to cash out, stock options tend to be less popular with private firms. While stock options can offer favorable capital gains treatment, most private firms choose SARs over stock options for equity incentive plans.

ESOPs have become a popular way to provide the benefits of ownership to rank-and-file employees while also providing a tax-advantaged exit option for existing firm owners. ESOPs are broad-based retirement plans that generally allocate employer stock to all employees (with certain exceptions) in the form of a retirement contribution. With an ESOP, employees earn stock in their employer over time, without putting in any of their own money, often building up a valuable nest egg for retirement.

An ESOP is a qualified retirement plan under ERISA, so it operates under strict regulations. The plan purchases stock from existing owners and allocates that stock over time to a trust account for the benefit of employees. Each employee earns stock in their account annually in proportion to their wages, similar to a 401(k) or profit sharing contribution. When the employee retires or leaves, the stock is cashed out, and the former employee can roll the proceeds into another qualified retirement account, or take the cash (subject to normal retirement account taxes and early-withdrawal penalties).

For sellers, an ESOP can provide much more flexibility and tax advantages over a sale to an outside buyer. The ESOP can buy some or all of the outstanding stock, and the sale transaction can be structured to optimize tax and other factors for the sellers. Employees get the benefit of indirect ownership without putting in any of their own money. And, the company gets tax savings that are not available to non-ESOP companies.

ESOPs have long been popular ownership structures among architecture and engineering firms. More accounting firms have been implementing ESOPs in recent years, with BDO being a high-profile recent example. Employee attraction and retention was one of the top reasons BDO cited in its announcement of the ESOP.

Likewise, firms in niche professions have found ESOPs attractive as a perpetual ownership model that provides an exit to existing owners while maintaining the independence of the firm indefinitely.

Direct Ownership, in which senior employees are invited to buy into ownership is a traditional partnership feature that is still relevant. Usually, this is reserved for senior employees who are invited to buy in after achieving certain performance criteria. In this way, it is a lot like “making partner”. However, with ownership decoupled from compensation, firm profits accrue to the enterprise, driving stock appreciation. This has the effect of both making the buy-in a meaningful commitment by the employee and incentivizing owners to grow shareholder value.

Buy-ins are usually financed by a note payable from the buyer to the company. This allows management to fine-tune the financing terms to make the buy-in more accessible, or more of a commitment. Profit distributions can help new owners pay down their purchase debt.

Some firms open up the opportunity to buy and sell shares to all employees with few restrictions. Usually the firm will set an annual price and a window during which employees can buy from or sell to the company. Some firms will also facilitate sales between employees. These plans tend to be rare for professional service firms because they encourage a short-term view and legal complications can arise with minority shareholder laws.

For a company that is driving shareholder value, direct ownership also offers an attractive retirement payout to owners. With good planning and staggered retirements, this model can be very stable, since buy-ins and redemptions are neutral to shareholder value.

Ownership Structures to Facilitate Growth Investment

Professional service firms have jumped into the M&A game with both feet in the last decade. M&A has taken on new urgency as a solution for both the talent crunch and the rise of disruptive technology. Tech for professional services began as an efficiency tool, evolved to become a competitive advantage, and now is becoming the price of entry. As the cost of staying ahead of the curve has skyrocketed, smaller firms are getting priced out, and economies of scale are becoming increasingly critical. At the same time, many firms are also paying out retiring Baby Boomers.

These trends are putting larger demands on capital to fund technology investments, strategic acquisitions, and partner retirements. This is making the practice of paying out all profits to partners unsustainable.

Firms are addressing this challenge with both structural and policy changes. From a policy perspective, decoupling compensation from ownership is key. Profits are no longer fully paid out. Instead, compensation is based on defined parameters by role and performance, with the goal of generating meaningful profits after all employees and owners are paid. This leads to growth in shareholder value and frees cash flow for investment.

While the economic benefits to the firm are obvious, such a change can have difficult cultural implications for senior employees. For junior employees, the change in compensation policy is economically neutral and culturally positive as it reduces the incentive for partners to leverage staff as workhorses to maximize partner profits.

As these employees advance, the new policy will become the norm. However, for partners used to their share of profits, there is no way around the fact that they will be taking home less. Structural solutions are required to offset this impact for former partners.

The first structural solution many firms implement is moving to a C-corp. tax structure. Partnerships that have built up debt to fund acquisitions and technology investment are in the uncomfortable position of reducing partner profit distributions to make debt payments. Adding insult to injury, partners are still taxed on profits that they don’t receive, since debt repayment isn’t tax-deductible. By switching to a C-corp., former partners are only taxed on the salary and wages they receive, thereby reducing, but not eliminating, the after-tax hit from lower income.

The second solution involves buyouts of some of the former partners’ interests. With greater ability to support debt as a result of profits from changing compensation as discussed earlier, coupled with profits to drive shareholder value, firms can help former partners monetize lost future income through a redemption of some or all of a partner’s interest. This may be financed with outside debt or with a note payable to the former partner.

As firms invite younger employees to buy in, this provides additional capital while committing employees to the firm and seeding ownership among the next generation.

Many companies are layering an ESOP into this mix to enhance both tax and employee retention benefits. BDO’s recent transformation from a partnership to a partially-ESOP owned corporation is a great example of this strategy.

With a leveraged ESOP, the company can effectively convert non-deductible debt repayment into tax-deductible retirement contributions. Former partners who sell to the ESOP have the potential to defer capital gains. And, in cases in which the ESOP owns 100% of the stock of an S-corporation, the company pays no federal income tax.

As we saw earlier, the ESOP can also be a great tool to attract and retain talent. In effect, an ESOP offers a two-for-one deal by using the same dollar to both buy out owners and to pay a retirement benefit to employees. The resulting tax deduction is the icing on the cake that can fund growth investment.

Ownership Models for Operating Flexibility

Partnerships’ obstacles to flexibility tend to stem more from cultural and policy factors than from structural, tax, or economic factors. The core issue stems from commingling ownership and leadership, which inevitably leads to decision by committee. The larger the partner group, the larger the committee. In stable market and economic conditions, this kind of broad engagement can strengthen trust among partners and foster organizational stability.

Today’s markets and economy have been anything but stable. Management by committee is becoming too slow for today’s rapidly changing landscape. Firms need strong, decisive, centralized leadership to stay ahead of shifting trends. Consequently, despite a trend toward broader ownership, leadership is narrowing. That means, many owners may not have a seat at the executive leadership table.

Corporations have long separated ownership from leadership. This is most visible in public companies, where anyone is free to buy stock on the public market, but, stock ownership is not a factor in an employee’s role in the company.

For many professional service firms, the days of herding cats are over. Instead of appointing managing partners who have to juggle firm management with client work, firms are hiring professional executives. Often recruited from the ranks of Fortune 500 companies, these roles include professional CEOs, CFOs, COOs and HR and IT executives, usually with no experience in the firm’s particular profession.

This frees the client-facing professionals to maximize their highest and best use, which is client service, rather than firm administration. It also creates a powerful leadership team, laser-focused on firm growth, strategic goals, and employee success.

Conclusion and Key Take-Aways

Firms are mixing and matching different structural ownership elements and layering policies on top of these ownership foundations that facilitate long-term strategic and cultural goals. While each firm is finding its own mix, the common thread is a decoupling of ownership from compensation and leadership. By creating options to strengthen talent attraction and retention, invest in growth, and create flexibility, this fundamental decoupling opens the door for firms to thrive in the dynamic environment of the 21st century.

How Adamy Can Help

This is a topic that is near to our hearts. We draw on our extensive experience helping business owners transition ownership as well as our own experience as a professional service firm. As curious life-long learners who enjoy helping clients solve meaningful financial problems, we are thrilled to brainstorm ideas and share our experience with you.

Contact us today

Contact one of our experts today to learn more.